Incorporating Scenario Planning into your Business Plan

RBC Small Business Talks uncovers the latest trends and insights to help owners navigate the issues & opportunities facing businesses today.

Businesses always operate under a certain degree of uncertainty, and planning for the “what ifs” is critically important. Scenario planning, which involves making assumptions on what the future will bring, can help you gain an understanding of how different situations – or scenarios – will affect your business. Allowing you to see alternate visions of the future, scenario planning can help you identify pitfalls, gaps and opportunities before they happen, and stress test your plans against a variety of situations.

In this webinar, Svendsen and Cummins discuss the fundamentals of business planning and how to incorporate scenario planning to help you start, run and grow a successful business.

Business planning basics

There are many reasons to write a business plan. And while some owners consider writing a business plan an overwhelming task, it doesn’t have to be. By breaking it down into individual steps, thinking through possible scenarios and developing an action plan to address them can help you express both the vision for your business and the way in which you can address various factors that may affect it along the way.

The very act of putting what’s in your head onto paper can help you articulate why your business exists, what it will bring to the market and provide clarity on how you should take action as your business develops.

As Cummins explains, she comes across two camps of entrepreneurs in her role as an entrepreneur coach. “On one hand, I see people flying by the seat of their pants and they’re fighting fires every day because opportunities keep coming up and they don’t know whether they should go after them or not. That is a sign of someone who hasn’t done that forward thinking of taking the time to articulate and create a critical path for their business,” he says. “Then I see people who have a business plan. They know exactly where they want to go, they have ideas on how to get there, they’re able to focus and use their time much more powerfully and strategically, and they tend to grow faster.”

Building scenarios into your business plan

While having a vision for your business’ future – and plotting it out in your business plan – is important, it is just as valuable to consider the obstacles and detours your business may face.

Thinking about and building solutions to account for a variety of scenarios can help ensure your business continues to move forward, even if it needs to take a few turns along the way.

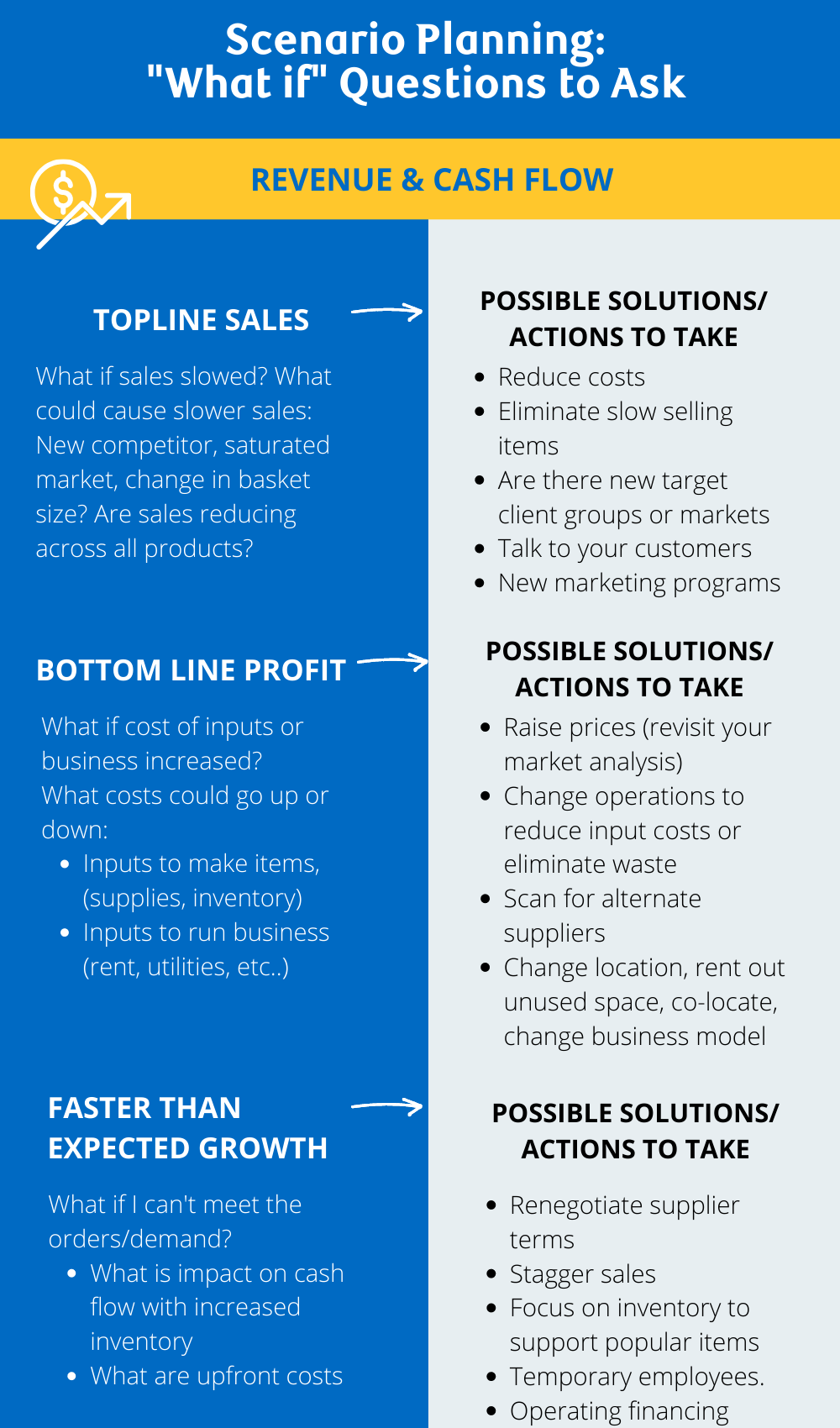

Scenario 1: Sales slow down

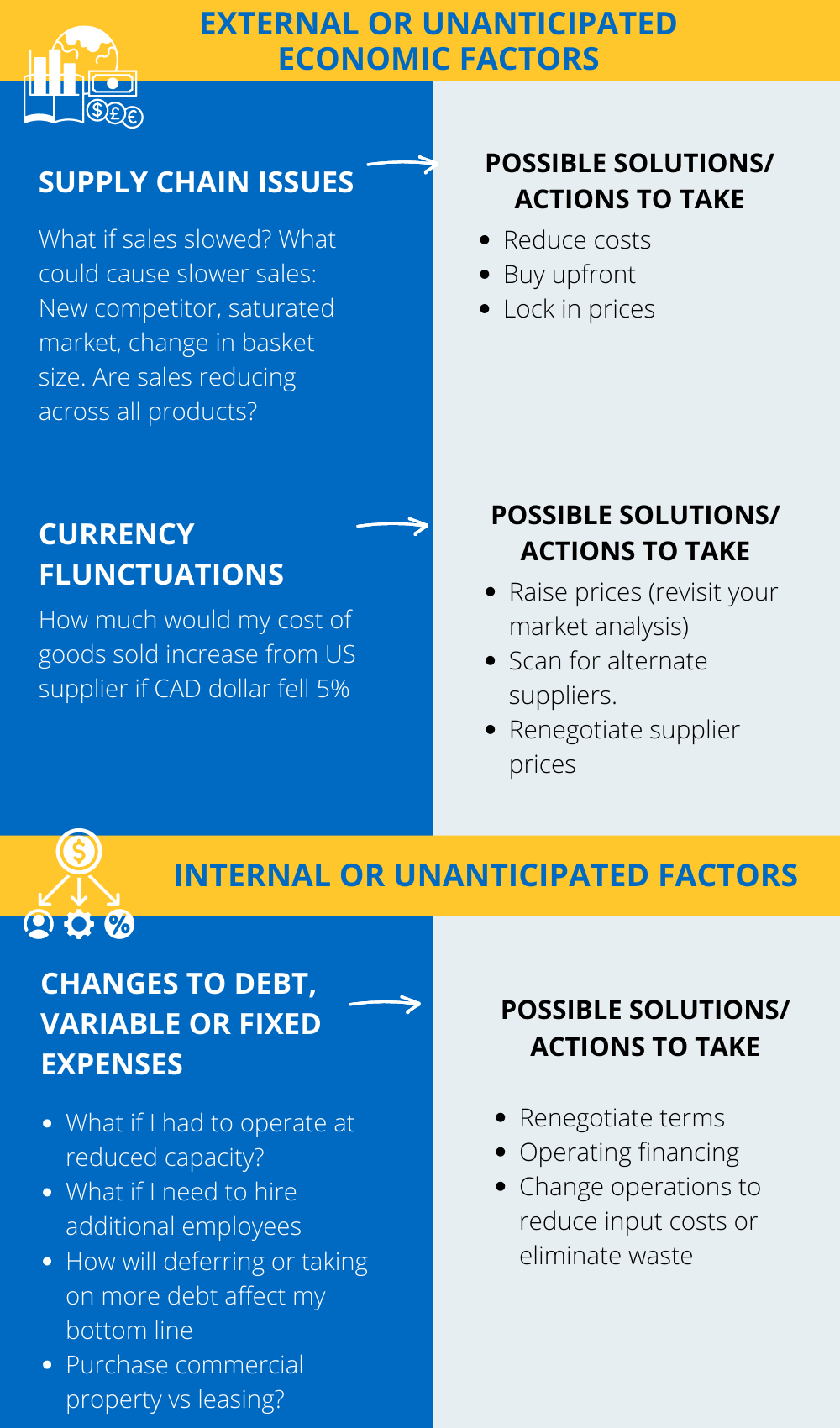

What if a new competitor enters the market and affects your sales? What if external factors affect demand for your product?

Possible solutions:

- To compensate for slower sales, consider reducing costs, buying product upfront and/or locking in prices to mitigate the risk of rising prices

- Eliminate slow selling items

- Talk to your customers to learn the root of slower sales

- Initiate new marketing programs to reach new client groups

Scenario 2: Profits take a hit

What if the cost of supplies or inventory increases? What if rent or utilities go up? What if the Canadian dollar falls dramatically, or interest rates rise?

Possible solutions:

- To offset a higher cost of doing business, it may make sense to revisit your market analysis and raise your prices

- Look for ways to reduce your input costs by changing up your operations

- Scan for alternate suppliers

- Looking at changing your location, renting out unused space or changing your business model to reduce your fixed costs

Scenario 3: Demand outpaces capacity

What if you can’t meet orders? What if you don’t have enough cash to cover upfront costs?

Possible solutions:

- Speak with your suppliers to renegotiate terms, allowing you to reduce your upfront cash outlay

- Hire temporary employees

- Monitor your inventory closely to support popular items

- Secure operating financing before you need it – so you don’t have to scramble for cash when the need arises

Identifying the “what if” questions that are most relevant to your business can help you anticipate and plan for the unexpected, and set your business up for success.

To learn more about building a strong business plan, expand the content below. You’ll find advice and insights discussed in this webinar and find out about tools that can help you develop and update your best plans.

The key components of a business plan

Explore these seven key components of a business plan, as discussed by Svendsen and Cummins:

1) Introduction

- If you’re submitting your business plan to an investor or financial institution, this is a really important section as it sets the stage for your audience. The introduction should include:

- A cover page

- A table of contents

- An executive summary

The executive summary is often considered the most important part of the business plan, as many investors will read it first – and it may influence whether they decide to keep reading. Svendsen’s advice is to write this last since it sums up the story you’ll tell in the rest of the document.

2) The Business Environment

In the Business Environment section, you will identify the external factors that could have an impact on your business. If you haven’t started your business yet, this section can include the research you’ve done so far. If you’re already operating, this is where you can talk about how long you’ve been in business, what you’ve accomplished so far, industry trends and growth prospects.

Cummins likes to ensure two key questions are answered in this section:

- Why are you/ your product/ your service needed now more than ever?

- Why are you the best person to provide it?

3) The Marketing Plan

As Svendsen explains, she has seen many owners focus on the “shiny objects” of marketing, particularly given evolving trends in social media. Cummins offers advice to owners considering their marketing efforts.

“The biggest thing to remember is that not all buyers are on TikTok,” she says, explaining the importance of knowing who’s buying from you and where they’re hanging out. If you’re trying to be on all platforms all the time, you won’t be able to be present or build the amount of content needed to fit all the parameters and algorithms.” She emphasizes the need to build good metrics to determine whether your efforts are worthwhile.

From a scenario planning perspective, Cummins recommends keeping close tabs on customers to ensure the product or service you’re providing is still meeting their needs. And if your customers are retooling (because they’re dealing with a pandemic or an uncertain economy, for example), planning for different scenarios enables you to retool your business to either meet their changing needs or to meet the needs of new customers.

4) Operations

The operations section of the business plan is the opportunity to demonstrate an understanding of your end-to-end business – how your product is made or how your service is delivered and how it gets to the customer.

Cummins emphasizes the need to outline your business processes. “If you don’t want to spend the rest of your working time doing absolutely everything within your business, you need a plan. It’s important to look for opportunities to make repeatable, automated and leveraged processes so you can be as efficient as possible with your time and focus on your zone of genius – that is, what is easy for you to do, but hard for others.”

Having a process written down enables you to detect vulnerabilities (ie, you may realize you just have one supplier for a key element of your business) and think through scenarios that can maximize your efficiency and therefore the output of your business.

5) Financing and Cash Flow Planning

Your finances section is a critical part of your business plan. The number one piece of advice Svendsen offers is to be realistic with your financial projections based on the scenarios outlined in the business environment section.

Cummins shares that one of the biggest things he notices is that business owners tend to underestimate the cost of running their business. She works by the 30/30/10 rule. “Right off the top, 30% goes into your tax savings bucket. Put it into a high-interest, compound earnings savings account so you have the money ready to pay your taxes,” she says. “Then put 30% into your operating costs, which will fluctuate depending on the type of business you have, leaving 10% for profit. When you start looking at your cash flow through this lens, you can start seeing how to allocate a budget.”

6) The Team

Depending on the type and size of business you run, your team can be just you, or it can be a team of people you’ve gathered around you. When it comes to hiring, Cummins offers these insights:

“I’m a bit unconventional when it comes to hiring, but if you’re the only one who is responsible for revenue or sales, one of your biggest opportunities is to hire someone who is going to strategically increase your revenue or sales so you can do more of what you do.” While many people will first hire assistants, Cummins recommends ‘hiring up’ versus ‘hiring down.’

“You can do your own emails for a while, you can answer your own phone. But when you can get someone to help you sell more, that’s a powerful growth engine for you.”

7) Risks and Conclusions

If you approach your business plan with a scenario planning lens, many of your risks will surface throughout your plan. These risks may include:

- What if you have only one supplier?

- What if your sales grow too quickly?

- What if the competitive landscape changes?

These are all risks to your business, which should be addressed as you build your plan. Other risks to consider include cyber risks, protecting intellectual property and cyclical or environmental risks that may play a role.

When you build your business plan, consider the various scenarios and “what ifs” that could affect your business so you can create alternate visions of what your future will look like and how you’ll get there. As consumers and business owners have experienced, life can change on a dime – but there is a real opportunity to be found in an evolving landscape.

“As entrepreneurs, we have the opportunity to be fluid, to shift and meet the market where it’s at,” said Cummins. Thinking specifically about today’s economic environment, she believes there is no need to wait.

“This is such a prime opportunity for small businesses. Some of the most powerful companies were built during recessions – we just need to take one step at a time and focus not on the negative but notice the opportunity that various situations and landscapes are presenting.”

Let Us Help You Build Your Business Plan

Building a business plan is a critical step to the success of any business – but RBC recognizes that it’s not always easy to do on your own. With the new RBC Business Plan Builder, you don’t have to. This comprehensive tool will guide you through a series of questions, offering resources and providing a framework for success. The business plan can be completed in as little as 30 minutes.

Try The Business Plan Builder Now >

RBC Small Business Talks uncovers the latest trends and insights to help owners navigate the issues & opportunities facing businesses today. We’ve made a recording available to all registrants, in case you weren’t able to join us or would like to re-watch the content. Please follow the link below:

Additional resources discussed during the event:

Missed our recent webinars for business owners? Catch recordings of all of our recent events here!

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. The information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by the Royal Bank of Canada or any of its affiliates.

RBC Small Business Talks uncovers the latest trends and insights to help owners navigate the issues & opportunities facing businesses today. Businesses always operate under a certain degree of uncertainty, and planning for the “what ifs” is critically important. Scenario planning, which involves making assumptions on what the future will bring, can help you gain…